"The Gleaners" by Jean Francois Millet, 1857

During the Middle Ages, European peasants worked land owned either by a wealthy nobleman or the church. The terms of their indentures required them to devote about 165 days of labor a year to their overlord. In the painting above, peasants gather grain that has fallen to the ground during the harvest process. The fruits of the harvest went to the land owner. The workers could keep what they managed to "glean" and grow a the small plot allocated to them. Russian serfs were required to devote some 150 days of labor to their overlord. Thus, the labor of these workers was "taxed" at a rate of roughly 44% (160/365). They were also periodically dragooned into their lord's army to fight wars they played no role in starting and from which they received no benefit. While this scheme allowed the nobility and church hierarchy to lead sumptuous lives, Thomas Hobbes famously described the workers' lives as "nasty, brutish and short."

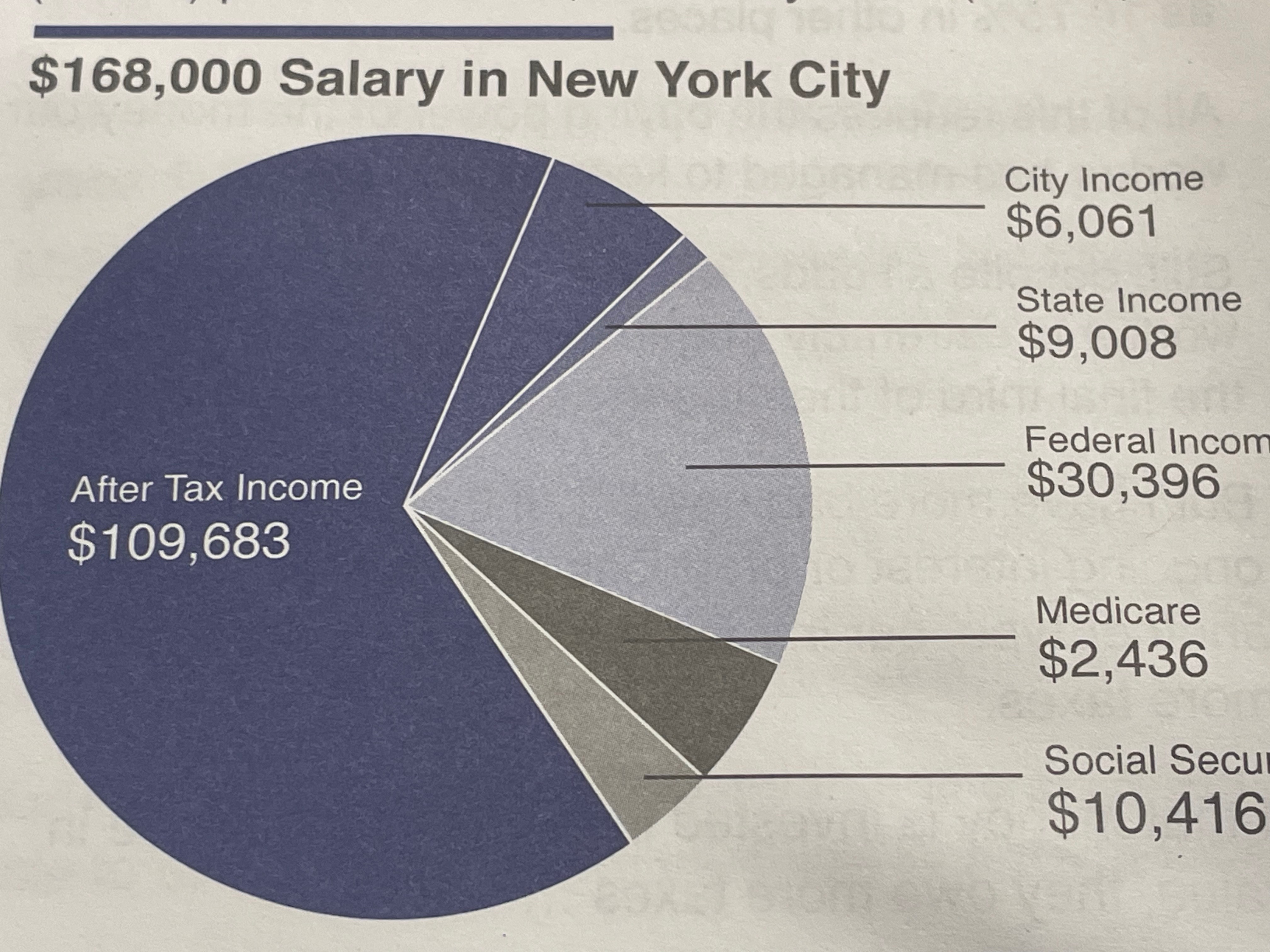

Today, life is infinitely better for workers - at least in the "developed" world. They can now acquire their own land and homes and choose their employer or become self-employed. But some things never change. The many still labor for the benefit of the few. Here is a chart from Weiss' Safe Money Report. It reports taxes paid by a hypothetical worker in New York City earning a very respectable $168,000 salary. It reveals that this worker's labor appears to be taxed at a rate of about 35% - 9% less than a medieval peasant.

Unfortunately, this chart does not tell the whole story because it fails to take into account other taxes imposed on the worker by his other government overlords. Let us assume that he (unlike most workers) saves 5% of the above reported "after tax" income. That would leave $104,198 to meet his living and other expenses. But, there are New York state and city sales taxes on goods and services (both 4%) that reduce his "after tax" income to $95,863. Then there is a real estate tax. This tax is either paid directly (by the home owner) or indirectly (by the renter). In 2022 the median price to buy a condo in Manhattan was $1.7M. A one-bedroom apartment was $710,000. Let us assume an average of $1.2M. The NYC real estate tax (1%) comes to $12,000. This reduces his "after tax" income to $83,863. Finally, there is the "invisible" tax - government created price inflation. Government officials try to convince us that it is now just under 3% but our prior writings show that number to be a hoax. It is more likely in the 8% range, reducing our worker's "after tax" income to $79,251. Thus, his total tax burden is 53% - meaning that he devotes 9% more of his labor to support his overlords than did a 16th century peasant.

The genesis of price inflation

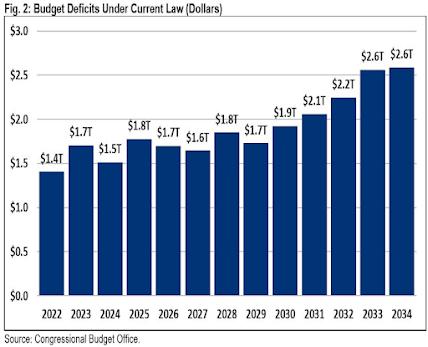

Our hypothetical worker's top overlord is the US government. It takes in tax money as "receipts" and spends it on "outlays." The Treasury's "outlays" have persistently exceeded its "receipts." The resulting "deficit" is papered over with additional borrowings (Treasury bond sales) and money created out of thin air by the Federal Reserve Bank. The bond sales run up the national debt while the printed money debases the currency. Here is a December, 2023 chart from the Congressional Budget Office reporting past and projected deficits.

The CBO consistently underestimates Congress' ability to spend money it does not have. In this chart it projected a FY2024 deficit of $1.5 trillion. The deficit was actually $1.8 trillion. The absurd premise of the CBO's deficit projections is that it assumes: a) there will be no new spending by future Congresses, and b) there will be no recessions for the next ten years. The former will, of course increase outlays and the latter will reduce receipts - both of which will significantly increase future deficits.

November 2024 was the second month of the US government's new 2025 "fiscal year." It spent $367 billion more than it took in. The October and November combined deficits total $624 billion. That works out to a $3.75 trillion deficit on an annualized basis. That number may be reduced over the next ten months. "Net interest" paid on the accumulated national debt in November was $79 billion (nearly $1 trillion annualized) and exceeds spending on the country's "national defense." Are these deficits cause for alarm? Those in government assure us they are not, despite the fact that the Congressional Budget Office recently calculated the national debt will soar another $20 trillion by 2034 - totaling $56 trillion.

Paying the piper

The Treasury currently pays an average 3.5% interest on its outstanding debt, much of which was incurred during times of low interest rates. However, rates have risen. New and maturing debt is being replaced with higher interest rate debt. If average interest paid stayed at the 3.5% rate, the Treasury would be required to pay nearly $2 trillion a year on the $56 trillion debt. If the average rate rises to just 5%, annual interest payments on the debt would be $2.8 trillion. Bear in mind that the Treasury's total receipts for fiscal year 2024 was just $4.92 trillion. If the nation's receipts remain steady (ignoring the chance of a recession) the nation's debt interest expense could consume 57% of its revenues. That would be catastrophic.

Of course, it will not get to the point of interest expenses consuming 57% of revenues because the system would first implode. To avoid that, governments-in-crisis always do the same two things to forestall their bankruptcies. The first is to raise taxes to nosebleed levels (that is, transfer ever more wealth from the people who earned it to the government that did not). The Brits are in the process of doing this now. The second is to further debase the currency. This allows the government to repay its creditors with cheapened money (i.e., defraud its creditors). Raising taxes and debasing the currency ensures pain for workers, savers and retirees. Elite political insiders will tell each other that, "you can't make an omelette without breaking some eggs." Unsurprisingly, it is never their eggs that get broken. How do we know it will work out like this? Because that is how government fiscal crises throughout history have played out. Noted author and economist Nassim Taleb, of The Black Swan fame, summarizes the problem. "So long as you have Congress keep extending the debt limit and doing deals because they're afraid of the consequences of doing the right thing...eventually you're going to have a debt spiral. And a debt spiral is like a death spiral."

In addition to much higher taxes and debased currencies, we can expect the Fed and other central banks to keep interest rates low to allow their governments to put off their day of fiscal reckoning despite the fact that artificially low rates (those below the commercially negotiated supply/demand level) always result in price inflation, as happened in the early 2020's. At some point in this process, the working classes that make up the vast majority of the population, may finally realize that they can no longer afford their government - any more than they can afford an unemployed, surly, adult offspring with expensive tastes living at home.

Most governments face the same problem

Virtually every "developed" country finds itself in a similar situation to the US. We recounted the many issues confronting England in our issue titled "The Decline of Empires". Voters there decided that a change in political parties was the solution to their problems. They voted in a Labor government. It proceeded to present a budget that has the nation in a state of shock and dismay with taxes to soar, making the country un-investable, negatively affecting employment and causing those who have accumulated wealth to consider fleeing that failing state. One indicator of the scope of the problem is that over half of the population (52.6%) now receive more in benefits than they pay into the state, per the Office of National Statistics, and the rapidly growing number of long-term unemployed on benefits. That is not sustainable. England also faces countless fiscal and social issues. Allister Heath at the London Telegraph provides confirmation that the British government has fully gone mad.

Given the intensifying culture wars, and the collapsing trust in our institutions, the fact that one of Britain’s leading conservative commentators is being investigated [by the police] for a post on X will unnerve many voters. Two-tier justice is real, in one fundamental way at least: Allison Pearson [a Telegraph journalist] is in trouble for an ancient tweet while the police rarely bother to track down stolen cars or mobile phones, even when presented with real-time geolocations or webcam evidence

Violence and disorder is rife and shoplifting has effectively been decriminalised, leading to the routine pillaging of supermarkets. Yet the state seems more interested in intimidating those accused of wrongthink.

It indicates a sinister power grab by an authoritarian elite that dismisses property theft as mere freelance redistribution and to whom free speech is synonymous with micro-aggression and oppression. What is certain is that this madness infuriates the right-thinking, silent majority like little else.

Our membership of the The European Convention on Human Rights has gone hand in hand with the collapse of our ancient liberties. We live in a country where thousands are now routinely deemed guilty in the most opaque of manners of “non-crime hate incidents” (NCHIs), an extraordinary, controversial concept originally formalised by the Blob, not by MPs through legislation. What has happened to our wonderful country? We used to be freedom-lovers, but we now apparently acquiesce meekly to the rise of authoritarianism and the normalisation of censorship. We need to speak out fearlessly, or else the Britain we knew and loved will soon cease to exist.

The Macron French government is in the final stages of welfare-state crisis following his desperate act of seeking, and failing to receive, a vote of confidence. The nation is riven with multiple political parties that cannot find any common ground upon which to proceed. What is needed, of course, is to dramatically slash the size and cost of the French leviathan state. That will not happen because those on the receiving end will not willingly agree to take less. It will take an existential crisis as happened in Argentina before the French government and its people come to terms with their problems.

Germany's Olaf Scholz followed Macron's ill-considered decision to call for a vote of confidence and he too lost. His government is near collapse and facing an election in the new year. Exports fell 2.8% from the prior month. The auto industry is in dire straits with its vaunted VW discussing shuttering three plants, laying off tens of thousands of workers and threatening to reduce the wages of those who remain. Bosch proposed to cut ten thousand jobs. Thyssenkrupp is to cut 40% of its steel division. Foreign imports are crushing auto producers that were strong-armed by the government into producing large numbers of EV's that are not wanted and cannot compete on price with much cheaper Chinese imports. The Bundesbank (German Central Bank) now estimates that 2025 GDP growth will shrink to just 0.2% over 2024 making it the worst economic performer in the G7. Scholtz is being pressed to drop his stance of limiting deficits to 3.5% of GDP as required by EU policy.

As with other nations, Germany's problems are self-inflicted. Bowing to the Green Party's demands, Angela Merkel closed all of the nation's nuclear power plants and spent 200 billion euros to develop intermittent wind and solar power sources that are incapable of supporting German industry and relied heavily on cheap imported Russian natural gas. After that gas was shut off following Russia's invasion of Ukraine, Germany was forced to import electricity and expensive liquified natural gas to heat and light its homes and power its factories. It now has some of the highest electric costs in the EU. Yet 77% of its energy consumption and 40% of its energy production still comes from fossil fuels and it is in no position to meaningfully reduce that any time in the foreseeable future.

The upcoming German elections are highly unlikely to address, much less solve, these long-festering problems. Sadly, Germany shows every sign of once again of becoming the "sick man" of the EU. Mises accurately summarizes the situation: "Germany does not have a competitiveness or human capital problem; it has a political problem." Compounding that, the Euro is near a 20-year low against the dollar causing Trump to threaten import tariffs on European goods. That would cause even greater pain on the struggling German and other EU economies. The falling euro and local weak economies also encourages European investors to redirect their money at the US economy, to the EU's serious disadvantage.

The Russian Central Bank has raised interest rates to 21% in an effort to stem soaring inflation resulting from massive money printing to fund its war in Ukraine. Russia has lost many thousands of young men who left the country to avoid being thrown into the meat-grinder war and many more thousands killed and injured in the war. Internal support for the war is divided, with supporters falling in number the longer the war goes on and as Ukraine brings the war home to the Russians through invasion and missile and drone strikes.

China faces mounting pressure resulting from its wasteful construction of millions of unnecessary apartment units to create jobs for workers and absorb the nation's massive steel production. After Chinese investors suffered losses in the local stock market, they loaded up on real estate. That real estate is now well down in value with few buyers in sight. Worse, many investors paid for units under construction and many of those units will not be completed due to the developers' bankruptcies. China suffers high youth unemployment that can lead to social problems. It has high local and national government debt and is loath to engage in much more "stimulus" spending, out of fear of igniting inflation that would inflame an already restive population. It faces stiff western tariffs to address its mercantilism (a strategy to increase its wealth and international power through highly aggressive trade practices) and faces a demographic crisis due to falling births and a growing elderly population that cannot be supported by the shrinking number of younger workers.

As Japan keeps its interest rate at .25%, the yen is near a fifty-year low against the dollar giving its products a big currency advantage over US producers but that may soon be offset by US tariffs that will threaten Japan's recent mild economic recovery. The country is still favored with a highly educated workforce and cutting edge products. Like China, it faces a declining birth rate with its attendant problems. Unlike Europe and the US, it has blocked immigration to maintain national cohesion, but that may have to change as demographics become an ever larger problem.

Canada's Justin Trudeau, leader of the formerly popular leftist government, has flirted with disaster for years. He is increasingly seen as high-handed and sanctimonious. The economy and government are on the brink following the resignation of his deputy finance minister Chrystia Freeland who quit and vocally criticized the government's policies and direction, especially his recent proposals for a sales-tax holiday on alcohol, junk food and other items, coupled with a plan to send $250 (Canadian) to everyone earning less than C$150,000. She called his tactics exactly what they are: "costly political gimmicks" to garner voter support.

Canada has also taken in a large number of immigrants (over 3 million) that bring with them all the related employment, housing, welfare cost, and social problems confronting the US, UK and EU. Canadians continue to face spiraling living and housing costs and a 6.4% unemployment rate. Trump has threatened to impose 25% tariffs on Canada and Mexico if they fail to stem illegal drugs and immigrants from crossing the US borders. This would also hit foreign producers that invested in plants in these countries in an effort to allow their products to enter the US under the terms of the liberal North America trade agreements currently in effect - but which are threatened by Trump. Trudeau currently polls 20% behind conservative leader, Pierre Poilievre, with 73% of voters saying he should resign - including 43% of his own liberal party.

Growing concerns for the US market

Ray Dalio, head of the world's largest hedge fund, Bridgewater Associates, has said for some time that the US economy and markets are headed for trouble. He fears a crisis "bigger than happened in 2008." Steve Blumenthal at CMG Capital Management lists in his newsletter, "On My Radar", the archetypal signs of a market crisis.

- Stocks are at record highs

- Valuations are at record highs

- Investors are concentrated in just a handful of companies - The Magnificent Seven

- Market breadth is deteriorating as measured by the number of stocks trading below their 200 day moving average

- We sit near the end of a long-term debt accumulation cycle

- Government finances are in horrible shape and

- Protectionism and restoring manufacturing is increasing.

John Hussman, former economics professor at University of Michigan and now principal at Hussman Strategic Advisors, recently wrote in the Financial Times,

Among several valuation measures setting record highs is one that has reliably been a gauge for the subsequent returns and potential losses of the S&P 500 index over the following 10 to 12 years: the ratio of the market capitalisation of US non-financial companies to "gross value-added" or corporate revenues generated incrementally at each stage of production. Since early 2022, this metric has rivalled and now exceeds the peaks of both 1929 and 2000. Returns are simply the inverse of valuations. When valuations are high, returns are low, and vice versa. All-time-high valuations indicate all-time-low returns from U.S. stocks. Stocks are just fractional claims on the future cash flows of the underlying businesses. The more you pay for the cash flows, the lower your long-term return.

Noted Swiss financial advisor, Felix Zulauf, fears that western nations are continuing to march toward "state capitalism" where the government dictates what industries will be supported with taxpayer money (i.e., the government chooses the winners and losers in the economy) through government bailouts, incentives and stimulus payments. This has repeatedly proven to be a failed system - Exhibit A being the old Soviet Union that collapsed in 1991 and Exhibit B, the Argentine government that collapsed last year. They fail because government bureaucrats are unable to replicate real capitalism where buyers and sellers of goods and services determine what should be produced and at what cost. State capitalism is a failed theory because the government is a "coercive institution run by a self-interested ruling class" (Mises) that always ends up ignoring the needs of the people in its zeal to feather its own nest. These developments create risk, a condition you must take into account to avoid being crushed. Howard Mark writes,

Investing consists of exactly one thing: dealing with the future. And because none of us can know the future with certainty, risk is inescapable...Thus, dealing with risk is an essential - I think the essential - element in investing. The first step consists of understanding it. The second is recognizing when it's high. The final step is controlling it.

By way of example, Palantir Technologies (PLTR) is a very popular tech stock. Its share price was recently 411X earnings (meaning it would take 411 years at present income levels to have earnings per share equal to its price). Is it a good company? In our view, yes. Is its price justifiable? Could it go higher? Of course. However, as an investor you must weigh all of your holding's risks. Are Dalio, Hussman, Zulauf and Mark wrong in predicting a coming crisis? We do not know and neither does anyone else. But they raise facts that are indisputable. You would be a fool to drive your car without insurance. You may never have an accident. But if you do, the injured party may take your savings and home away from you. Prudence also calls for "controlling" (hedging) your investment risks. Are you doing that? If not, the time to start is now.

The Fed's implementation of Quantitive Easing (a euphemism for "vast money printing") ostensibly to aid workers had an effect - but not the effect most people believe. Former Senior Fed economist Dr. Lacy Hunt writes that QE "exacerbated the income and wealth divide." Stanley Druckenmiler, billionaire investor, philanthropist and chairman of Duquesne Capital, adds "the biggest accelerate of wealth disparity has been QE." Carl Sokoloff writes, "QE was socialism for the 1%." The mainstream press has wholly ignored this result, covering up for those responsible for QE's perverse outcome of pushing up prices for assets held by the already wealthy.

While the Fed's 40% increase in the money supply lined the pockets of the wealthiest, it ignited the highest price inflation in forty years. It is always those lowest on the financial totem pole who suffer the ravages of inflation the most. Another ignored effect of QE is that it allows the US government to fund endless wars (Iraq, Afghanistan, Ukraine, Gaza) and permits it to continue to spend money well beyond its receipts, for a time - but not forever.

Is there any place to hide?

Many people tout the benefits of crypto currencies, claiming that no government can "print" them, so their value cannot be debased and that continued demand for them will increase their value. While that is correct, there is another feature that gets little press coverage. Crypto currencies can be stolen. Not only can hackers break into ledgers and wallets to steal your cryptos, governments can and do seize them as well. There have been several reports that North Korea has been active in stealing cryptos. It recently hacked over $1.3 billion in coins. The FBI has boasted about seizing bitcoins from "criminals and terrorists." If it can seize their bitcoins, are yours really secure? If the US government follows through with its plan to replace cash with a digital currency, it will almost assuredly forbid the holding of other digital coins in order to force adoption of its new crypto currency. Governments do not like competition for their fiat currencies because that allows people to avoid the routine seizure of their money through currency inflation.

Bonds are nothing more than IOU's. You give your money to the issuer and it promises to return it to you at some time in the future, plus interest. If it defaults, you may get nothing. Yes, US Treasuries will always be paid because the government can print any sum of dollars at will and at no cost. But the worth of those dollars 5, 10, 30 years in the future is unknowable. However, the last 100 years proves convincingly that they will be worth far less than the dollars you give to the Treasury today. That is why some call them "certificates of confiscation."

Stocks are the traditional place to put money to make it grow and every investor should own some. Of course, companies go bankrupt on a regular basis, even companies that are believed to be "sure bets." Recall Lehman Brothers, for example. It was once believed that if you invested in the "Nifty Fifty" stocks during the 1960's and 1970's they were a "sure thing." However, many fell on hard times. Today's "Magnificent Seven" stocks are also not bulletproof. Stocks, carefully selected, can be a great investment, but as you age, their risk becomes your biggest challenge. Following a major market set back, you may wait a very long time to recover from your loss as the next chart shows.

Source: GoldSilver.com

If you are in your 50's, 60's or 70's, having to wait 6 or 14 years to recover from a 40-50% market loss would keep you awake at night for the duration. One that takes 29 years to recover would be catastrophic. Never over-weight your stock holdings. Discuss your stock allocation with your trusted investment advisor. If he or she tells you not to worry about such things because the Fed will always step in to "save the day," look for another advisor.

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com and clicking on the “Subscribe” button. We will not share your email with anyone.

Important Message: The foregoing is not a recommendation to you to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance. © All rights reserved 2024