THE DECLINE OF EMPIRES

History is rich with failed empires: the Roman Empire, the Inca Empire, the Mongol Empire, the Macedonian Empire, the Ottoman Empire, the Spanish Empire, the Russian Empire, the British Empire. Though each stood atop their world for a period, they all fell prey to the same cause. They became overextended and could no longer support the cost of their empire even after extracting tribute from their defeated enemies and colonies. Their end often came suddenly.

The Decline of the American Empire

Today, the US struggles to maintain the empire status that it achieved following World War II. The US takes great pride in claiming that it is "The Indispensable Nation" that has not just the right to interject itself in other nations' business but the duty to do so. It maintains over one hundred military bases around the world and fancies itself to be the "World's Cop". Unlike early empires, it does not take tribute from other nations. Instead, it loads all of its empire costs onto its own taxpayers - and those willing to lend money to the US. It took the US government nearly 200 years to accumulate its first $1 trillion of debt. It now adds that much every few months - with the current total approaching $36 trillion.

Debt can accumulate for a long time before creditors become nervous and demand repayment. The US has been able to grow its massive debt because it has had the "exorbitant privilege" of issuing the world's "reserve currency". It has been able to import valuable foreign goods in exchange for its devaluing dollars. Foreign producers historically invested many of those dollars in US Treasuries that were considered to be "risk free". That era is coming to a close. What sane foreign producer would buy a 10-year or 30-year US Treasury instrument whose value is guaranteed to drop precipitously before maturity? This chart from the St. Louis Federal Reserve Bank shows the dollar's loss of purchasing power just since December 2020.

With rising interest rates, the US Treasury has been issuing many more short term bills and notes than long term bonds. Uncharacteristically, the short term Treasuries bear a higher rate of interest than longer term issues, further discouraging buyers from signing on for the long-term debt. This is like borrowing money from your credit card issuer in order to pay this month's minimum balance. Your debt swells rapidly until it suffocates you.

As the world awaits the outcome of the 2024 US presidential elections, neither of the political candidates has expressed any plan for addressing the nation's increasingly dire fiscal situation. There is one certainty. Whoever wins the election will continue to spend far beyond tax revenues, thereby enlarging the already staggering national debt - that will never be honestly repaid. The scheme is to continue to debase the dollar so that US bond holders will be repaid in devalued dollars. No politician will admit this constitutes a bond default, but that is precisely what it is. Throughout this process, the middle and lower classes will be further beggared by rising prices and taxes. The moment of crisis arrives when the working classes finally realize that what they call "inflation" (rising prices) is actually a carefully crafted scheme to shift wealth from them to the government and its insider controlling political elite. What then? That will be the nation's day of reckoning.

Older Americans remember being taught that the Founding Fathers warned against becoming involved in political and military alliances because they always draw countries into foreign wars. Americans like to believe that the US is a "peace loving nation" focused on its own growth and development. This vanity ignores the country's sorry history. The US has engaged in nearly 400 military actions between 1776 and 2023 - with more than half of them occurring since 1950 and over 25% (100+) since the end of the Cold War in 1991 with the collapse of the Russian government. Each of these adventures incurred a cost in money and lives. Over the twenty year period Nov, 1955 to April 1975), the US spent hundreds of billions of dollars in Viet Nam and lost over 58,000 US lives (with 1241 soldiers still missing in action). Many tens of thousands of Vietnamese, both North and South, lost their lives as well. Once US voters finally tired of that war, the US government announced victory and quickly abandoned South Vietnam to the rapidly advancing Communist forces of the North.

Having learned nothing from that terrible waste of human life and national wealth, the US embarked on another twenty year war in Afghanistan that ran from October 2001 to August 2021 at tremendous cost in lives and money after which the US again abruptly departed - this time leaving a billion dollars worth of military equipment behind for the Taliban's use. 2,459 US lives were lost together with many thousands of Afghans. The US lost another 4,620 lives and more wealth in its war in Iraq that ran from 2003 to 2011. These actions underscore Randolph Bourne's observation during World War I that, "War is the health of the state". Politicians quickly learn that war allows the government to divert the nation's attention, manpower and resources to an outside "enemy" thus keeping the local voters from focusing on their own increasingly dysfunctional government.

That dysfunction is clear in the US. Here is a chart showing the massive US budget deficits (just the first ten months of each year) that must be funded with higher taxes, more bond sales and more money printing by the Federal Reserve Bank. The Congressional Budget Office estimates a $1.9 trillion budget deficit for this fiscal year - and that is premised on no further increases in spending in the next months and no decrease in government revenues. The US national debt has increased by $12 trillion just since Q1 2020.

The Formerly "Great Britain"

England has a glorious history founded on the successes of many generations of capable political and military leaders, great thinkers and hard working people. Not so long ago it was the preeminent empire ruling over a large swath of the world. But like all empires that have gone before, it too found a way to fritter away its many advantages and squander its accumulated wealth. The challenges it now faces are numerous and, possibly, intractable. Brits would like to believe that there is still a leading role for them to play on the world stage but reality is setting in and proving that to be a pipe dream.

All nations face multiple challenges. They either overcome them or fail to do so. The former continue to thrive while the latter fall by the wayside. The UK's challenges today are daunting. All that can go wrong is rapidly going wrong. Like former empires, it is failing because it promises to pay for everything for everybody ("bread and circuses") in order for its politicians to buy votes to get elected to office. Such is the inherent flaw in "democracy". Voters eventually learn that they can vote themselves largess at the supposed expense of everyone else - not realizing that in the end, they pay for everything the government does. Tax revenues fail to keep pace with expenses, deficits become unmanageable and the government is forced to devalue its currency to keep the plates spinning for a while longer. England's Harris tweed jacket is rapidly unravelling before their eyes.

The country's problems include: health, education and welfare expenses that are soaring ever higher, uncontrolled immigration that is placing enormous financial burdens on cities, villages and the state, the nation suffers from housing shortages and high prices, rising worklessness, rampant social "wokery" (insistence on equal outcomes for all regardless of unequal knowledge, skills and effort), the Leeds riots, frequent discharges of sewage into waterways, impractical and unaffordable green goals, falling energy production and rising utility costs due to greater reliance on intermittent power sources, growing dependence on foreign nations for electricity, oil and gas, crime going unsolved and unpunished, early release of violent criminals due to overcrowded prisons, ever rising taxes and fees, endless increase in regulation and restrictions on the shrinking producing portion of the economy, a falling birth rate, recent high and unfunded pay raises for public employees and NHS workers with no commensurate increases in their production, promises of vast new housing to be built in "green zones" (small towns and rural areas) forever changing their historic character, VAT taxes on private school tuition forcing some to close and push more students into crowded and underfunded public schools, nationalized industries that have no incentive to be cost efficient or to provide reliable services, falling out of the top-ten manufacturing nations for first time since the Industrial Revolution, a 19 billion pound budget black hole, the National Grid forecasting coming electric blackouts, decaying roadways and infrastructure, and 9.4 million 16-64 year olds deemed "economically inactive" (neither working nor looking for work with many receiving benefits and contributing nothing to the nation).

Following ill-advised Covid school closures, 30,000 children under five are receiving benefits for severe behavioral disorders and there are surging diagnoses of autism and ADHD. In 1992, 2% of working age adults claimed disability benefits, today that number exceeds 6% with the biggest increase in claims for mental health issues. A PwC survey reports that more than a million 18-24 year olds claim to be struggling with their mental health (22% of the Gen Z age group!). And 53% of the population are now net recipients of government (taxpayer) support. Thus, the minority of the population is now supporting the majority.

It is fair to note that the recently empowered Labor party inherited these problems that have been festering for years but its proposed solutions do not begin to address any of them and simply seek to paper them over with yet more publicly funded programs and subsidies. This will rapidly accelerate the fiscal calamity to come. Rachel Reeves (new Chancellor of the Exchequer) is calling for steep rises in taxes that will cause further out-migration of the wealthy leaving the soaring tax burden to fall more heavily on the working classes. The critical fact is that the working and productive classes did not create these problems - ill-advised government programs and policies did the damage, yet the proposed government solutions are simply more of the same. The Telegraph aptly capsulizes the problem.

Big Government is the enemy of its people - The key growth destroying features of the social democratic (populist) experiment are bigger government, higher taxes, and an ever-shrinking private sector to get those taxes from. It's a patten with only one eventual outcome: national bankruptcy. For most of this century the UK has been increasingly drawn into that doom loop.

The question is whether the people now leading the UK government comprehend the scope of the problem and have the will to shrink government and lower taxes thereby leaving more money in workers' pockets, rather than subsidizing them with more handouts. The short answer is "No". Governments never volunteer to shrink. Recent proof is Argentina. The former government grew massively and consumed an ever larger slice of the national pie with its populist agenda. It largely funded its operations by printing money that rapidly became worthless, beggaring the nation's workers. Finally, the people recognized the cause of their problems and voted the socialist government out of office and installed Javier Milei as their new president. He ran on a platform of taking a "chainsaw" to government and has done so. The result has been falling inflation and, amazingly, recent budget surpluses. He has had to battle the fervent resistance of those in government who are desperate to maintain the status quo ante. His work is not complete but the people of Argentina can now see the benefits of slashing government and taking back more control of their own lives.

Will the people in England learn from Argentina's example? Not likely. Serious changes in government rarely occur until circumstances pass into crisis mode as they did in Argentina with over 100% inflation eating the nation alive. Even then the outcome is never certain. Recall that the French Revolution started with the best of intentions of eliminating the power of the entrenched nobility in favor of Liberté, Égalité, and Fraternité, but before it was over the people endured the Reign Of Terror. The Russian revolution also did not end with "The People" in charge. Upon the collapse of the Russian government in 1991, control of the Russian government and most wealth were seized by the Oligarchs. That happens because the insider elite recognize the opportunity to gain power and wealth for themselves at the expense of the public during crises. What the English (Americans and all of Europe) desperately need is their own Javier Milei to hack back the government kudzu that has smothered their economies.

A Sorry State of Affairs

In our last issue we wrote about the US government's manipulation of data to present a warped picture of the state of the economy. We argued, for example, that the "jobs reports" were being falsified to make the current administration look good. Soon after that issue was released, the Bureau of Labor Statistic finally admitted that it had "overstated" new jobs by 818,000 over the last twelve months - a whopping 30% exaggeration. This is a rare example of candor from the Department of Labor and it only happened because many were challenging the accuracy of its reports.

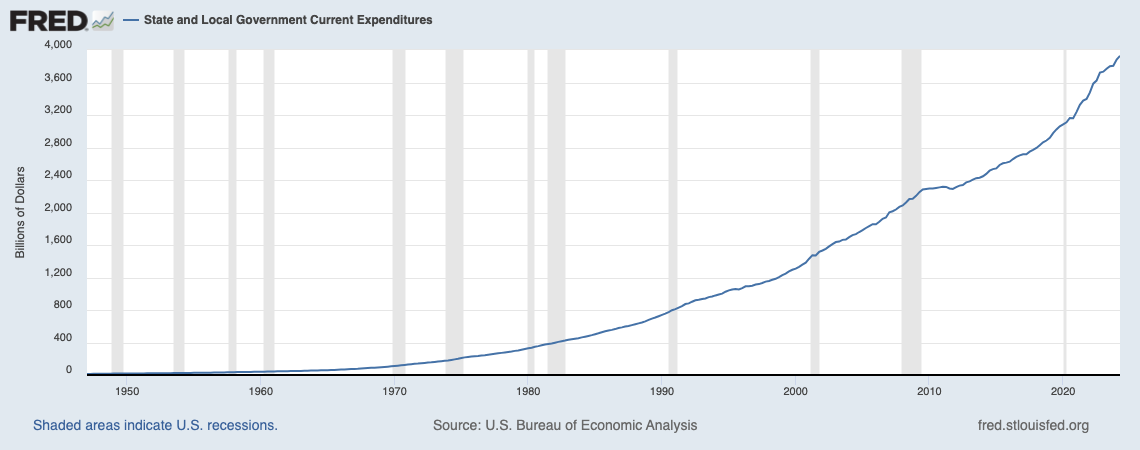

Some data is harder to misrepresent but rarely finds its way into the main stream media. For example, the combined federal, state and local budget deficits are running at a rate of 8% of GDP. Note that these are deficits. Actual spending at all government levels amounts to an astounding 40% of GDP. The first chart below reports the growth of state and local spending (now nearly $4 trillion) and the second one reports the soaring cost of federal spending ($7 trillion). GDP is roughly $27 trillion.

Long gone are the days when we could trust Congress and the president to enact sound economic policy, the kind that could expand the percentage of Americans who are getting ahead and flourishing. You know, policy that includes basic fundamental tenets like sound money, balanced budgets, smaller government, moderate regulation, and free-market trade and economies.

It has often been said that "People get the government they deserve". If they end up with an oppressive, confiscatory government it is because they have passively allowed that situation to develop. However, they have the choice to either accept that fate or reject it. Knowing his history well, US founding father Thomas Jefferson wrote,Instead, we have a huge, sprawling government with massive debts and deficit spending, no accountability for whether our tax dollars are spent wisely, and an ever-increasing appetite to dole out more subsidies to garner votes.This election, there's even socialist talk of price controls for food, something that has never led to an increase in prosperity – not once – in the history of mankind.The truth is, we can't rely on the government to enact sound economic policy because it's simply not in the politicians' best interest.

The concept of government is that the people grant to a small group of individuals the ability to establish and maintain controls over them. The inherent flaw in such a concept is that any government will invariably and continually expand upon its controls, resulting in the ever-diminishing freedom of those who granted them the power.When the Government fears the people, there is liberty. When the people fear the government, there is tyranny.Whenever any form of government becomes destructive of these ends, life, liberty, and the pursuit of happiness, it is the right of the people to alter or abolish it, and to institute new government.

He presciently warned in 1787 that,

The tree of liberty must be refreshed from time to time with the blood of patriots and tyrants.

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance. © All rights reserved 2024

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com and clicking on the “Subscribe” button. We will not share your email with anyone.