WHO PAYS FOR THIS MONETARY MADNESS? (Spoiler Alert……. It will be you)

We are not predicting an imminent financial crisis. But what has transpired over the last decade ensures that we will suffer major pain at some point. It is difficult to wrap one’s arms around what has happened since the 2008 sub-prime mortgage debacle. But what has happened during just the last year is astonishing. If you tally up all the money the Fed has ever printed, over 40% of it was printed in 2020.

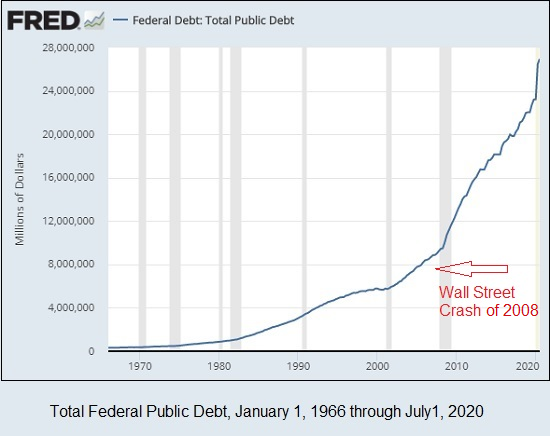

In just three months, the U.S. government grew its budget deficit by more than the past five recessions - combined - and the Fed bought more Treasuries in just six weeks than it did in 10 years under Ben Bernanke and Janet Yellen. US government debt as a percent of GDP will explode from 64% in Q2 2008 to over 120% by the end of this year.

On an operational basis, the US will collect about $3.8 trillion in taxes and other revenue this year. It will spend 10% of that on interest on its existing debt (at the lowest rates in history) and about $5 trillion on “transfer payments” (depending on how many more “stimmy” checks, bailouts of state and local governments, payments to people in prison, college loan forgiveness, “shovel-ready” infrastructure projects, and other hand-outs are passed by Congress).

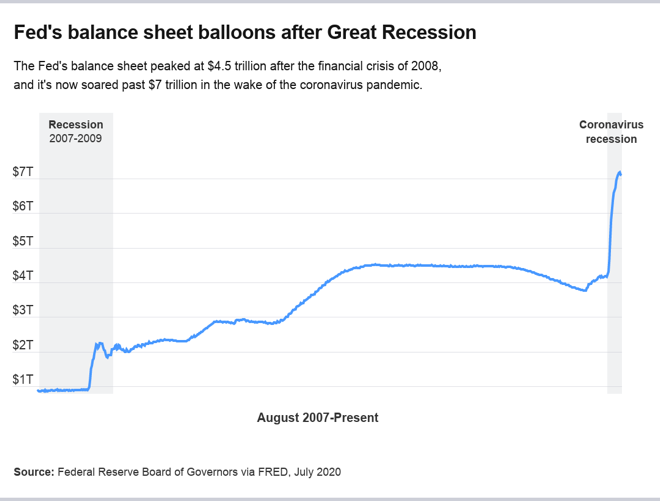

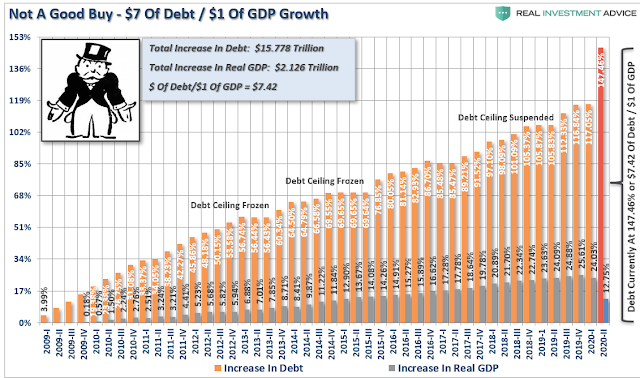

The chart below shows that the government has supported the US economy with enormous quantities of printed money for the last twelve years and despite that massive stimulus, GDP growth has been pathetic.

All the while, the Fed and government officials continued to tell us that the economy was improving and they have everything under control. The obvious fact is that the economy was kept on life support with continuous injections of financial adrenaline. But for those, it would have rolled over. Each time the Fed even hinted that it might back off, the stock markets cratered and the Fed was forced to renew and expand its monetary support.

Current political thinking in the US and elsewhere is that we can continue to “stimulate” the economy by amassing ever larger debts - without consequence. Some refer to this as Modern Monetary Theory (MMT). Others refer to it as the Magic Money Tree. There is nothing modern or magical about the theory. Throughout history, governments have been spending money they do not have. Rome, Spain, England, France, Russia, Venezuela, Argentina, Italy, and Greece quickly come to mind.

While the Fed and Congress assure us that there is no long-term price to be paid for their soaring budget deficits and perpetual bailouts, every sentient being knows that is not so. Were you raised in a family where you were taught that “There is no such thing as a free lunch?” Then you understand that someone always pays. Our much touted “free public education” is not free. Residents pay for it through real estate or other taxes. “Free school lunches” are not free. Taxpayers pay for them. “Free medical care” is not free. Someone pays the doctor’s and nurse’s salaries and the costs of running the clinics and hospitals. Housing subsidies, food subsidies, education subsidies are all paid by someone. There is no benefit provided by any government to anyone that is not paid for by others. The price might not be readily apparent, but it is always paid by someone. If you are employed or have taxable income, that “someone” is you.

During the bursting of the 2000 tech bubble, the Fed could have stood aside and allowed over-indebted, profitless dotcom companies to fail so that scarce resources could be redirected to viable companies. The creditors of those failed companies and the shareholders would have suffered losses but the economy would have regrouped and moved forward. Instead, the Fed flooded the economy with cheap money allowing failing businesses to borrow at negligible rates and continue to survive as “zombie” businesses (unable to even pay the interest on their loans with earned income). As a result, we have an economy still saddled with decade-old, loss-making businesses.

The 2000’s easy money from the Fed turbo charged the subprime bubble. When risk-taking bankers were threatened with bankruptcy, the Fed again rode to their rescue bailing out Citigroup and many others (including foreign banks). A few entities were cast adrift, but most of the insiders were bailed out with trillions of taxpayers’ dollars. The Covid lockdown has had the same result. Banks and businesses are being bailed out with more trillions of dollars of Fed created money.

Investment advisor and author John Mauldin writes,

I have been writing for many years that the US in particular and the Western “developed” world in general were approaching a time where none of our choices would be good.

We have arrived. Any choice the government and central banks of the US and the rest of the world make will ultimately lead to a crisis. Just as the choices that Greenspan and Bernanke made about monetary policy created the Great Recession, Yellen and Powell’s choices will eventually lead us to the next crisis and ultimately to what I call The Great Reset.

I believe we have passed the point of no return. Changing policy now would create a recession as big as Paul Volcker’s in the early ‘80s. There is simply no appetite for that. Further, the national debt and continued yearly deficits force monetary policy to stay accommodative.

Where are the journalists who should be investigating and reporting on this building crisis? They are AWOL. Bill Bonner explains,

No weight-loss expert was ever invited onto the Oprah show to showcase his new book, Don’t Eat So Much.

Nor did any household finance book, with the self-explanatory title, Save Your Money, ever make it onto the bestseller list.

And if you are waiting for an economist at the Federal Reserve to tell colleagues to “back off and let the economy do its thing,” we hope you are not holding your breath.

The nation passes its time watching reality TV and hoping the Fed and Congress will find a painless way to save our bacon. That is not going to happen. Congress has utterly failed us and left the Fed to sort it out. Wall Street on Parade,

What really changed the course of economic history in the United States and put the country on its debt-fueled disaster course is the Wall Street crash of 2008 and the bailouts, both monetary and fiscal, that have followed ever since, together with the unwillingness of Congress to confront this reality.

The failure by Congress to separate the giant federally-insured banks from the Wall Street casino, that is, to restore the Glass-Steagall Act, thus making perpetual Wall Street bailouts unnecessary;

The failure by Congress to strip federally-insured banks of the ability to hold tens of trillions of dollars notionally in dangerous derivatives, thus making perpetual bailouts unnecessary;

The fear by the Fed of allowing another stock market crash because consumers might retrench from spending if their 401(k)s implode;

The failure by Congress to restore corporate pension plans to workers, thus allowing loyal, productive U.S. workers to live in dignity in their retirement years and de-linking the wealth effect from the stock market and 401(k) plans;

The failure by Congress to conduct meaningful forensic investigations into how Wall Street’s Dark Pools, High Frequency Traders, and mega banks have joined forces to become a fraud monetization system and institutionalized wealth transfer, creating the worst wealth and income inequality in U.S. history.

What dangerous path has Congress and the Fed taken us down? This chart graphically tells us.

Note the small blip during the 1940’s. That reflects deficits incurred to fight WWII where the US was embroiled in multi-year wars in Europe, Africa, and Asia. The waterfall on the right side of the chart was to respond to the sub-prime crisis and Covid. Berkshire Hathaway’s Charley Munger warns, “We’re in uncharted waters…Nobody has gotten by with the kind of money printing now for a very extended period without some kind of trouble. We’re very near the edge and playing with fire.” Is Charley an alarmist?

CGM Wealth recaps some of the problems we face:

Interest rates are near zero and negative in some parts of the world. The result? Recessions will be more frequent and more painful.

MMT has begun. Nobody has gotten away with the kind of money printing that’s happening now without some kind of trouble.

Felix Zulauf sees U.S. debt topping $40 trillion.

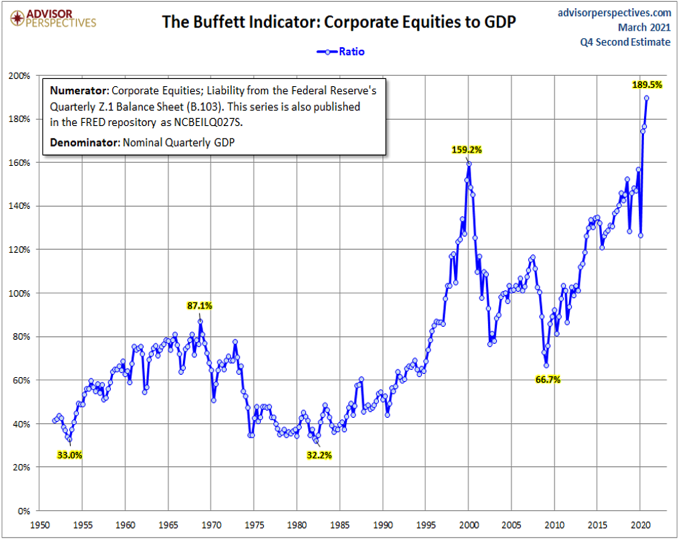

Valuations have never been higher. Market cap relative to GDP (Buffett’s favorite), market cap relative to domestic income, sales to earnings… etc.

Forward return probabilities are lower than they were in 1999. The decade that followed lost about 1% per year. It took nearly 15 years, 2000 to 2015, for tech to get back to breakeven (inflation adjusted).

The quality of debt has never been worse—especially in the European Union, as member countries are handcuffed by a flawed monetary structure. Many US corporations are in equally rough shape.

We’re seeing a near-record level of zombie companies: they compose 15% of corporations in the U.S., and an estimated 20% of corporations globally. They’re fueled by zero-percent interest rate policy and investors’ desperate search for yield. This will end badly with default levels spiking in the next crisis.

We’ve got record margin debt. The system is uber leveraged. Leverage is risk.

The aging demographics in the western countries, Japan, and China are not favorable conditions for growth.

The gap between the haves and have-nots is widening. Mix slow growth, low wage growth, and higher costs of goods into the equation and people aren’t going to know what hit them, but they will feel it.

A rising superpower, China, is challenging a declining superpower, the United States.

Bottom line: The current boom is the third great bubble of the past quarter century. We are heading down the same path as the dot.com bubble of the late ’90s and the real estate bubble that burst in 2008.

You can quibble with one or more of these problems but you cannot ignore them all. What options do the authorities have at this point? Graham Summers writes that the Fed’s choices are few. They can,

Allow bond yields to rise, which will blow up the debt markets, triggering a horrifying crash worse than 2008, or,

Let the U.S. dollar collapse.

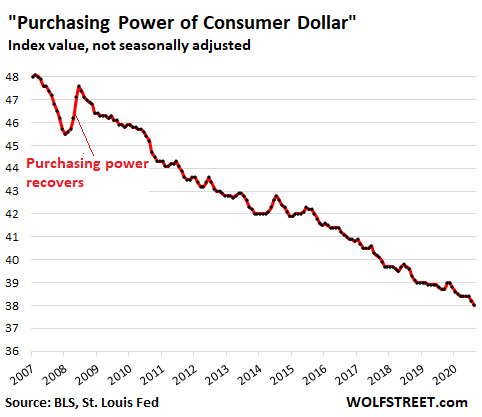

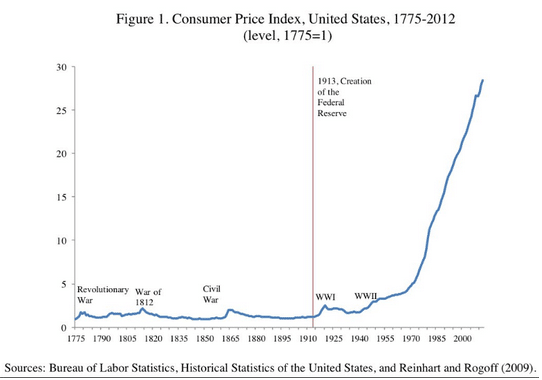

The data are clear, irrefutable and alarming. They have already chosen No. 2 as the next chart reveals.

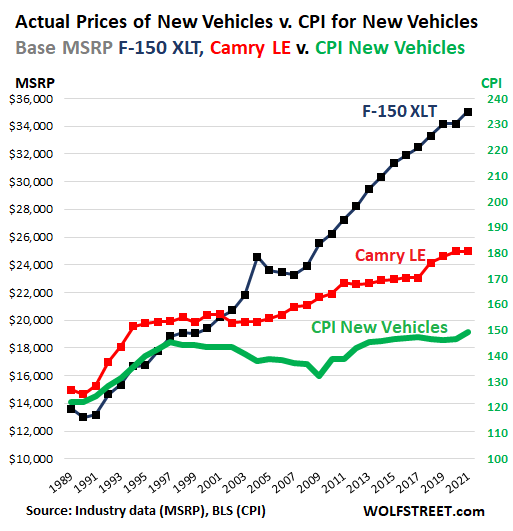

The Fed assures us that the government-calculated Consumer Price Index confirms low inflation and the public take them at their word. Are stable prices your personal experience? The CPI reports a modest rise in prices for “new vehicles” but actual prices refute that gross misrepresentation.

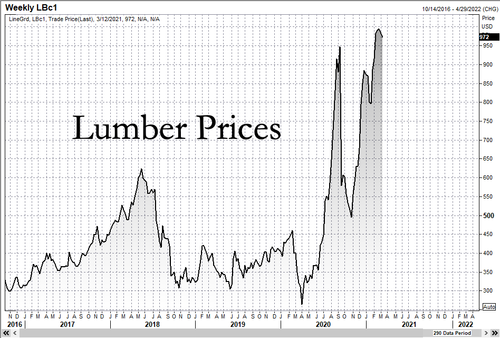

Most family’s biggest monthly expense is housing and the largest input for new housing is lumber (30% or more). House prices will necessarily rise.

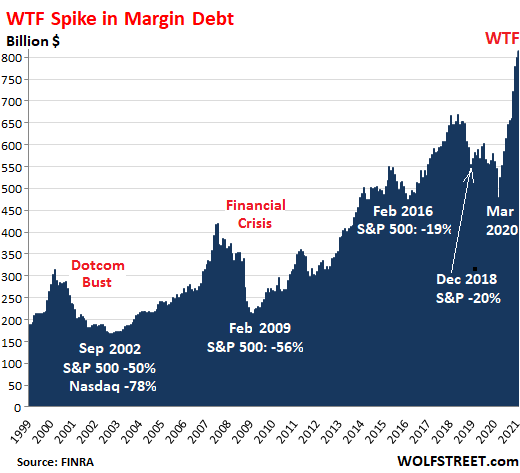

Renown value investor Jeremy Grantham from GMO writes that the Fed’s monetary expansion has “finally matured into a fully-fledged epic bubble” with the usual signs of idiocy and parabolic acceleration. He notes that it is an odd bubble. Prior bubbles at least occurred during an economic boom and had a believable narrative. This one does not. The current bubble is occurring during a lock down of the economy. Nevertheless, margin debt for stock traders is at record levels.

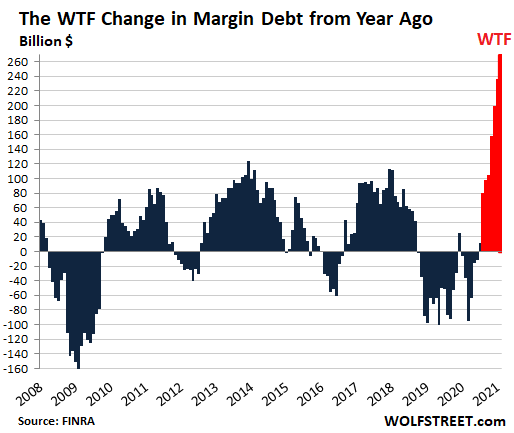

The increase in margin debt, year-over-year, is off the charts.

Financial editor, Ambrose Evans-Pritchard at the Daily Telegraph, notes his concerns:

It was Irving Fisher’s “permanently high plateau” in 1929 after the advent of assembly line manufacturing; or Alan Greenspan’s hopes in the late Nineties for a step-change in the economic speed limit, led by information technology – akin to the leap forward with the steam engine.

This time there is … what exactly? Trade is contracting. Globalization is in retreat. The US economy has been ravaged by Covid and there will be plenty of scarring. Yet the S&P 500 is higher than before the crisis hit.

Structural economic change is almost invariably painful, but the repeated lesson of history is that it is best not to try and get in its way; the sooner such change is allowed to take its course, the sooner resources are released to invest in the new, allowing the economy to transition to a different and hopefully better form.

Yet governments nearly always attempt to obstruct it. Voter pressure inevitably makes saving the past a more pressing political concern than galvanizing the new.

Rewind to Seventies Britain, and we see a case study in what not to do when companies and even whole industries become uncompetitive and therefore unviable.

Huge amounts were spent supporting lame duck businesses and sectors; it delayed the reckoning, certainly, but only made it very much more painful when finally, it was ushered in under the deliberately cleansing policies of one Margaret Thatcher.

That very same, political choice is once again fast approaching.

The Fed is confronted with the classic “Debt Trap.” If it cuts back on stimulus, the economy craters. If it raises rates, the economy craters. So, it is forced to continue with stimulus even though the amount of debt is already past the point of no return. The Treasury is forced to issue ever more debt to service the ever-growing debt and pay for the budget deficits. The Fed will be the buyer of last resort for Treasuries. Who else is going to buy a 10-year Treasury paying 1.65% interest when the real inflation rate is 8%?

There is only one way out for the US (and most other governments). The value of the currency will continue to fall. When that happens, the price of foreign goods will soar unless every country with whom the US trades devalues in lock-step with the US. It will be chaotic, at best.

For every government bond there is a creditor who holds it as an asset. Think pension funds, insurance companies, private investors, trading partners, the social security funds, and others. If rates rise dramatically, these holders will suffer huge losses at redemption or sale. David Stockman explains,

Central banks all over the world, including the Federal Reserve, have an aspirational goal of 2% inflation. If you are age 30–40, that means every dollar you save today will lose half its value by the time you need it for retirement. And that’s what passes for planning by a committee. They literally plan on destroying the value of your dollar. The only real debate is over how fast to destroy it.

If Greenspan had raised rates because of rising inflation starting about 2003–4, there would have been no housing bubble, no subprime crisis, no overheated stock market, and no stock market crash. We would not have had the worst unemployment numbers since the Great Depression. Retirees and everyone else would have been able to earn reasonable yields on fixed income instruments. (Emphasis in the original)

Thanks to years of [Fed] mistakes, Powell is locked into a policy trajectory that leads nowhere good but also can’t be changed without enormous pain. In summary, nothing is really going to change in terms of Federal Reserve policy. It will keep using broken data to justify its loose monetary policies, the monster deficits will require them to purchase even more Treasury bonds and, given their presuppositions, they really have no choice. They will continue on that course until there is a crisis, and then they will double down.

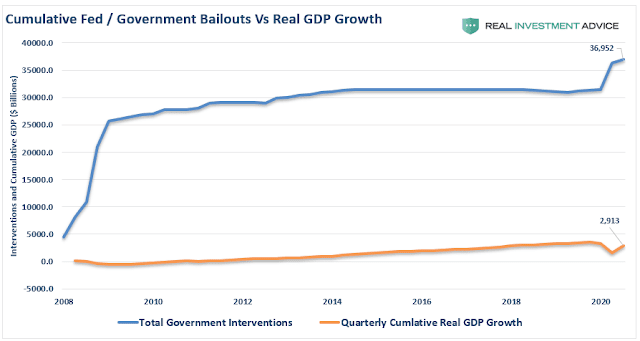

The US now spends $7 to “stimulate” $1 of economic activity. It does not take a financial wizard to see that this is the road to perdition.

All this creates huge risks for us. Our problem is that we overestimate our risk management skills, unjustifiably confident that the situation won't get away from us. Think back, were you caught short in 2000, 2008 and again in March 2021? Then you will be caught short again by the next crisis unless you find a way today to hedge the growing risks to our economy and currency that will present themselves in the future.

The “Buffett Indicator” compares US stock prices to national GDP. Current levels are unhinged.

Beyond stocks, there is evidence everywhere suggesting that we are in an epic bubble market. For example, the digital “artist” known as "Beeple" sold one of his “works,” that exists only in restricted digital form, for $69 million at an online Christie's auction. The work is titled "Everydays – The First 5,000 Days." It is a digital collage of all the images that Beeple (real name, Mike Winkelmann) has posted online since 2007. Unlike other works of art, the unknown owner cannot look at it on his wall or table top. All he can hope to do, like a GameStop shareholder, is sell it to a bigger fool.

On February 19, “artist” Chris Torres sold a digital artwork called "Nyan Cat" for nearly $600,000. The work, also an NFT (non-fungible token), is a crude digital drawing of a cat with a Pop-Tart body, flying with a rainbow behind it. Do these signal a market top to be followed by a market collapse? No one knows because the future is unknowable. But we should take reasonable measures to prepare for that possibility.

Charles Hugh Smith at oftwominds.com, tries to focus our attention on risk:

Systemic risk is difficult to isolate and analyze, so we're literally blind to it. It's not that we're blithely ignoring risk--we simply do not see it. We're flying blind through jagged mountain tops we can't see through the thick fog of false confidence.

There are several reasons for our innate difficulty in discerning risk. One… is recency bias: the natural assumption that the recent past is a reliable guide to the future. This leads us to underestimate the risk of non-linear financial-economic dynamics.

Linear means increasing or decreasing inputs to the system generate equivalent outputs: doubling the input doubles the output, and so on. Non-linear means modest changes in inputs generate outsized changes in outputs.

It's not easy to discern the potential for non-linear dynamics until they emerge, typically with surprising speed. This is why stock market crashes catch the vast majority of punters off-guard.

Central banks and governments have gone to extreme lengths to maintain the illusion of linearity, but these extreme measures have generated emergent properties beyond their control. This illusion of linearity implies a control of dynamics so perfect that no linear situation can ever become non-linear. This is the illusion of godlike control

In other words, we assume the authorities (The Federal Reserve, etc.) have godlike control which limits the risk of things spiraling out of control (i.e. non-linearity).

“Non-linear” and “emergent properties” are concepts taken from chaos theory that explains how minor changes in input can cause massive changes in output. Nassim Taleb described this phenomenon in his book “Black Swan.” It is an event that no one sees coming because the non-linear result deviates so dramatically from the input.

While we know that the Fed and other central bankers do not have God-like control over their economies and markets, we find it difficult not to follow what the herd is doing (party on!). This is because: a) we do not want to miss out on more hoped-for profits (greed), b) we do not know what to do to protect ourselves (lack of knowledge), or c) we take comfort in believing that the Fed will save the day (naivete).

Dr. John Hussman writes that, “Extraordinary monetary policy has one function, and it is to amplify yield-seeking speculation when investors are inclined to speculate. That and that alone, is how quantitative easing has impacted the economy in recent years.” If the Fed wants us to take on risk and engage in excessive speculation, then we know our way forward is to de-risk - sell our more speculative holdings and find safe harbors for the proceeds.

We need safe harbors because governments are forced to devalue their currencies to service their massive debts and/or to protect their exports. Thus, bond holders will be big losers whether interest rates rise (your bond loses value) or rates are repressed (your bond loses value).

Mr. Bonner minces no words in opining how the US (and for that matter the UK and EU) got to this point.

America’s economy is not really capitalist. It is a form of late, degenerate state-controlled, crony-manipulated, empire-addled, pseudo-capitalist claptrap.

A quarter of the economy is directly run by the feds. Another quarter – including medical care and education – is guided and approved by them. And the remainder is chock-a-block with rules and regulations… All of them intended to upgrade, or at least to genetically modify, the fruits of naked capitalism.

We don’t know what America would look like if capitalism were permitted. But it would certainly be a whole lot richer. Especially the working stiffs.

Socialism is always a drag on an economy. And the more the feds decide who wins and who loses, the more they tilt the playing field to favor their friends, cronies, and the Deep State elite.

What does a “late stage, degenerate state-controlled, crony-manipulated, empire-addled, pseudo-capitalist nation” look like? It looks just like this:

Which is a simple way of showing that our “stores of value,” (dollars, pesos, euros, etc.) have become increasingly worth less and this often leads to a financial crisis. Mr. Bonner describes one.

At the end of the 1990s, as a major financial crisis in Argentina approached, people tried to protect themselves by hoarding cash. Some kept pesos. Some kept U.S. dollars. Some kept bonds. Some kept pensions.

All of these paper savings and investments proved disastrous.

The peso was cut loose from the dollar. This caused the peso to fall by 65%.

Dollar deposits were no protection; the government merely closed the banks and converted dollar deposits into pesos. Same losses.

Pensions and bonds were marked down similarly… or the companies went out of business for 100% losses.

Later, private pensions were taken over by the government (supposedly for the purpose of protecting retirement funds). The government used the private pension funds to buy its own bonds.

Lesson: Paper assets can be too easily manipulated and devalued.

The result of this was devastating to the middle-class savers who counted on them. Many were wiped out. At the peak of the crisis, many former middle-class families were forced to dig through trash cans just to find something to eat.

The rich, meanwhile, were shrewder. They kept much of their money in foreign accounts – especially in Uruguay and Miami. And they bought real estate, businesses, and collectibles, instead of paper assets.

Do you see huge deficits and ever more “stimulus” in your future? If so, then you know that savings, pensions, government benefits, and life insurance proceeds, will all continue to lose purchasing power and should either be avoided or hedged.

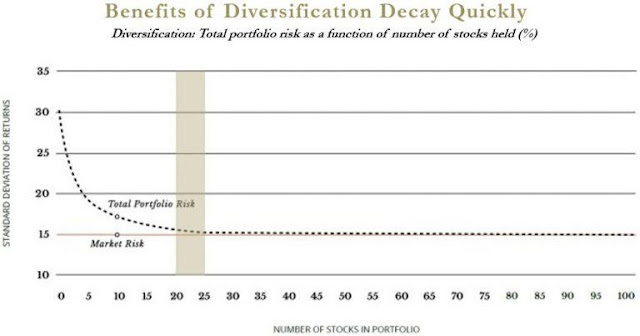

If stocks are at bubble levels and bonds are a disaster in the making, what to do? Advisors tell us the answer is to “diversify” our investments. That does not mean what many people believe. Some think that the more stocks they own the more diversified they are. That is only true to a point.

Your advisor has also likely warned you not to become overconcentrated in any one asset or asset class. That too is good advice. If you are a US reader, when you review your portfolio and other assets what do you see? US stocks, US bonds, and US real estate? Think about that. It means you are 100% concentrated in US dollars. For many decades that was a very smart bet. It is less of a smart bet today. The US is no longer the top economic dog and the dollar is no longer a reliable store of value. We need to look outside the box and consider other ways to diversify.

No investment plan is bullet-proof. When the world economy abruptly shut down last year, virtually all asset classes suffered, at least initially. The best you can do is to be diversified in different asset classes and in different political jurisdictions. Remember the Argentine saver who suffered far less when she held assets outside of Argentina in a foreign account and in a foreign currency. That money could not be frozen, devalued, involuntarily converted to pesos, or confiscated. A foreign account also allows her to own stocks and other assets denominated in foreign currencies, further diversifying her holdings as well as generating foreign currency income.

People rarely think of cash as an asset class, but having some set aside is what allows you to buy assets at a discount following a market sell-off. If you are fully invested you have no money to pick up bargains and must wait – sometimes years – for your investments to recover. Of course, the down-side to most cash is that it is no longer a good store of value. It is a wasting asset. As your government devalues your currency, you lose purchasing power. However, there are some currencies that do better than others, even during crises, such as the Swiss franc. For generations, people oppressed by their spendthrift governments have exchanged their failing currencies for francs. They can be held in a Swiss investment account that is not difficult to set up.

Other asset classes that should be considered are precious metals, real estate, art, and other collectibles. Jim Rickards writes that throughout history, prudent wealthy people invested “1/3, 1/3, 1/3.” One third in real estate, one third in gold and one third in art. Every asset class has pros and cons to ownership and each responds differently during financial crises. Some are highly illiquid like real estate and art. If you needed money urgently you would not get fair value for them. Gold can always be sold on the world market but not instantly. Only cash satisfies your need for instant liquidity. How much? That depends on your personal needs.

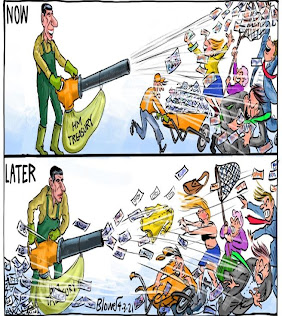

While it is a certainty that most currencies will continue to be debauched, that is not the only cost we will pay for our governments’ mismanagement of our economies. Their knee-jerk reaction will be to raise taxes. Below we see the UK’s Chancellor of the Exchequer, Rishi Sunak, happily flooding the British economy with “stimulus” but later realizing he must suck it back in taxes. There is no free lunch.

The bottom line is this: If we do not take charge of our future in a timely way, future events will take charge of us. We need to do it now because we have no way of knowing when the next crisis will arrive. Did you know in January 2020 that the US would be shut down for a year? We did not know it either. But it happened. So, while we always hope for the best of times, we must plan for the not so good times.

*CPI as it was previously calculated to reveal the growing deception.

© All rights reserved 2021

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance.