Political and Market Cycles

We are all familiar with the aphorism that, “those who do not know history are doomed to repeat it.” But even those who do know history are often doomed because they convince themselves that “this time is different.” Some events occur infrequently, so we are repeatedly surprised by and unprepared for them, like recessions, pandemics, and social unrest.

We recently experienced chaos at the Capital and last summer’s BLM marches cum riots. Are they harbingers of things to come? They both demonstrate growing and widespread frustration with the status quo.

President Peron on his inauguration day.

Davos Man is trembling. The cosmopolitan superclass is scrambling for ways to share a little of its income stream – as a prudent insurance policy – before the bottom half of western democracy takes matters into its own hands. Staggering inequalities have festered, to the point where the average chief executive of an S&P 500 company earns 357 times as much as the average non-supervisory worker. The ratio was around 20 in the mid-1960s. It was still 28 at the end of Ronald Reagan’s term.

These are informed, intelligent, thoughtful people who are warning us that a nation bitterly divided between the few haves and the many have-nots will not endure.

The US Economic Crisis

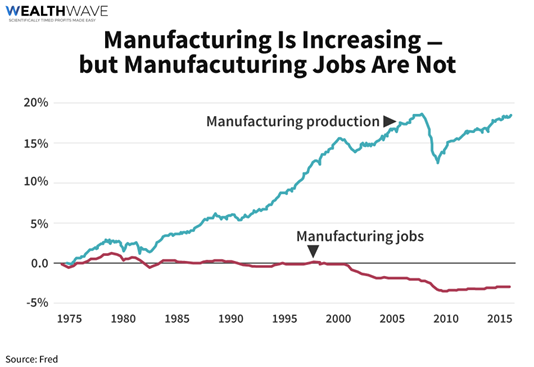

It is said that the US is recovering faster from the pandemic than is Europe. That sounds like good news except for the fact that the EU is a disaster. More important, the US is not recovering nearly as fast as its biggest competitor, China. The undeniable fact is that the US is no longer the global industrial leader. It was once the workshop to the world and was its biggest creditor. Now it is the world’s biggest debtor boasting a $28 trillion national debt and more than $120 trillion in off balance sheet future liabilities (e.g., social security, federal pensions, Medicare, military medical care and pensions). This fall from grace took place over many decades and with the active participation of both political parties.

The 2020 US budget deficit was over $3 trillion and that will be exceeded this year if Biden’s spending plans are enacted. Today, instead of sending our goods around the world and reaping the profits, we import someone else’s clothes, computers, cell phones, furniture, housewares, fruit, autos, etc. No politician has offered any credible plan to address this escalating problem. The usual bromide that the US will “grow its way” out of this mess is a fantasy. How can the US pay off its existing debts if it continues to run multi-trillion-dollar annual budget deficits?

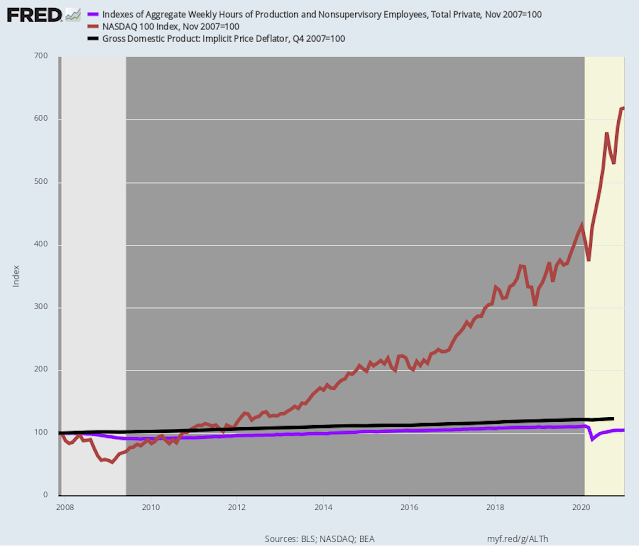

The black line below shows the minuscule “growth” of the US GDP. How do we square that lack of growth with the rapid growth in Nasdaq stocks shown in red?

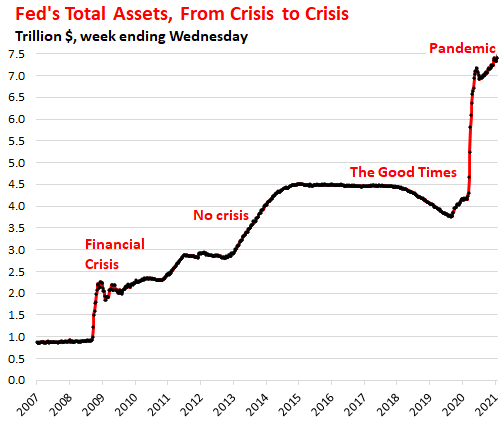

This GDP/Nasdaq disparity can be easily explained. The Fed added trillions of dollars to the economy. Those dollars found a home in the markets. Did that flood of money increase revenues commensurate with the increase in stock price? If not, then these stocks are overpriced and will, at some inopportune time, revert to their real value as recently happened to GameStop. Following a meteoric ride from $15 to over $450, it is now at $50.

Some people have argued that the GameStop event is proof that the “little guy” can take on the big guys. That is nonsense. Robinhood traders were paying, $100, $200, $300 and up to $450 a share in order to “stick it to the man” (the hedge fund shorts). How are those folks doing now that the stock is back at $50? Most lost everything that they put into the trade and those trading on margin lost much more. So, who “won”? It was the hated hedge funds. Senvest Management LLC raked in a cool $700,000,000 on GameStop from the Robinhood traders. This is a classic example proving that wildly overpriced assets will always return to the mean and hand huge losses to those who were suckered in on the way up.

Financial writer John Mauldin takes the Fed to task for inflating these asset bubbles.

With Janet Yellen and Jerome Powell both in the mix now, I can’t imagine how this ends well. US Treasury yields are the benchmark for all kinds of other financial asset prices. If they aren’t floating freely, the entire global economy is basically one giant price control. The result…will be widespread resource misallocation and asset mispricing. And eventually a “repricing event” that will make the recent GameStop fiasco look like a child’s tea party.

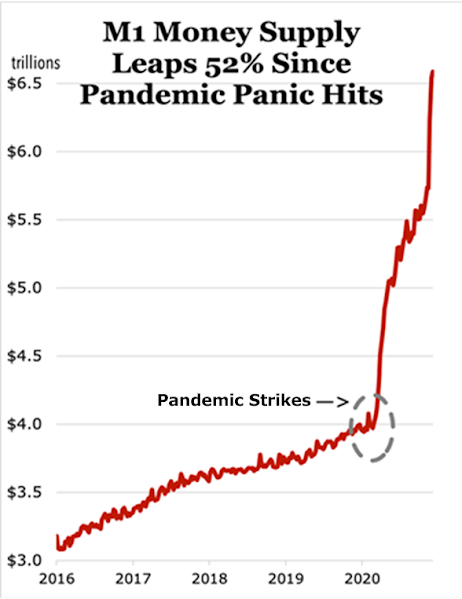

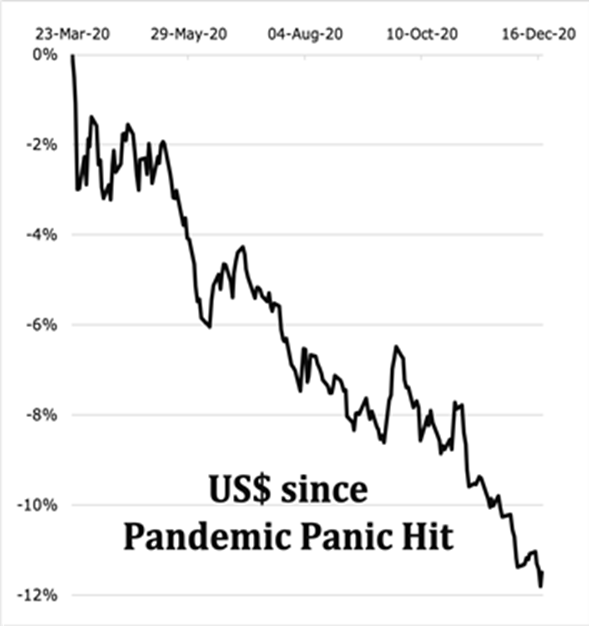

In addition to asset bubbles, another result of the Fed’s vast money printing is its negative effect on the value of the dollar and thus, most everyone’s salaries and savings.

This is a chart of the US dollar index (the dollar against a basket of our trading partners’ currencies). Our trading partners will not take this lying down. They will be forced to adjust the value of their currencies downward in order to protect their own economies and exports. Yellen has warned that she will not tolerate other nations’ doing so. That is to say, the US is free to drive its currency down by reckless money printing and thereby gain a trade advantage but anyone else trying that will be branded a “currency manipulator” and punished with tariffs.

As the former head of the Fed, one might think Ms. Yellen has special insights into the workings of our nation’s economy and is in an excellent position to sail us safely through the shoals of the Covid financial crisis. Prepare to be disappointed.

In the spring of 2018, she announced that, “You will never see another financial crisis in your lifetime.” That reveals her unjustified belief that the she and the Fed are infallible in reading the economic tea leaves and have both the means and skills with which to nip every crisis in the bud. Very recent history refutes that belief. In its panicked response to every crisis, the Fed is a one-trick pony: it prints staggering sums of money.

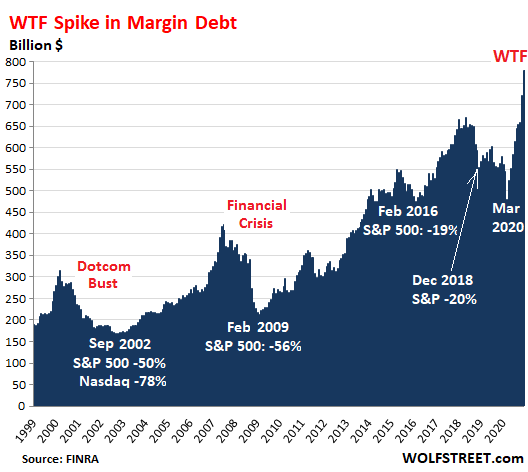

This surge of money always encourages unjustified risk taking in the markets that then viciously correct. There are many warning signs of this, such as the new extreme level of margin debt. This has always led to tears.

This risk taking creates the disconnect between asset prices and valuation realities that we see in almost every asset class. For example, the Australian dollar, New Zealand dollar, and Canadian dollar are at levels not seen for years, and with no fundamental or technical bases to justify those valuations.

Upon examination is it easy to see that the US economy is fundamentally broken. Blogger Wolf Richter describes it as follows,

The Weirdest Economy Ever, driven by stimulus, forbearance, bailouts, record money printing, record government-deficit spending, exuberant financial markets, and record low costs of funding. It has evolved into a system that is destined to fail.

Financial writer Andy Kreiger asks us to consider this question:

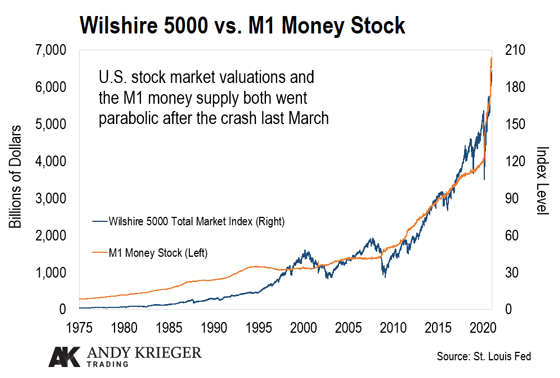

Does it make sense that, with over 20 million people still receiving some form of unemployment insurance, our stock markets should be rising parabolically and moving farther away from long-term averages than ever before? This is not the sign of a healthy market. It is unsustainable, and it is dangerous. When the bubble deflates, it will unleash an awful wave of bankruptcies – both personal and corporate – that will wreak havoc on our economy. Therefore, the central bankers will try to somehow keep the bubble inflated while praying that inflation doesn’t rear its ugly head before their term is up.

Bill Bonner describes the price we will pay for the Fed’s actions:

Jesus could turn water into wine. But the Federal Reserve can go one better… It can turn worthless pieces of paper into – money! Trillions of dollars’ worth of money. Enough to “stimulate” the world’s biggest economy into a state of transcendental ecstasy. This is the big story of the 21st century… the fantasy of fake money and the subsequent real-world, real-time butt-kicking that Americans will get as a result.

Of course, today’s conditions do not have to end in disaster. A crisis is not foreordained. We have options. All it takes is for earnest people to run for and be elected to office on the platform of fewer handouts to citizens and businesses, a smaller military, fewer foreign entanglements, less regulation, sound money, and greater protections of our personal liberties. However, if does not come to pass then you better get to work on developing a Plan B.

Below is a link to a terrific Bloomberg interview of famed investor Jeremy Grantham. He has been around long enough to have seen almost everything. He discusses extended valuations, SPACS, monetary policy, emerging markets, metals, Bitcoin – probably everything that is on your mind. https://youtu.be/RYfmRTyl56w

The EU Shoots Itself in the Foot, Again

Due to the bureaucratic incompetence that is endemic to the EU, the task of getting people vaccinated has been a disaster. Ursula von der Leyen’s government wasted weeks approving and then ordering doses of the vaccines. The Union will suffer needless deaths and a delayed recovery.

The EU was touted as a free trade zone but once adopted it quickly metastasized into an authoritarian central government that insists on having its thumb in every pie. Columnist Allister Heath is unflinching in his criticism,

It is no longer possible to deny that the EU is a power-hungry, unethical bully. It waged a five-year war of attrition against British democracy… Brussels doesn’t care about peace in Northern Ireland. It has no real interest in genuine free trade: its concern is merely to extend its jurisdiction and legal and political supremacy… At a time when Brexit Britain is taking moral stances on Hong Kong and Alexei Navalny, the EU continues to suck up to the Russians… At best, the supposed European superpower intends to act as some sort of amoral non-aligned player, friendly to China and happy to take NATO handouts in return for nothing…

The EU was meant to be the antithesis of Trumpism: it was billed as a law-governed, humanist Rechtsstaat. In reality, it is incompetent, uninterested in the rule of law, threatening and autocratic… A 70-year experiment has failed: there is no longer any justification for the people of Europe to continue to allow themselves to be governed by these apparatchiks... The EU will stagger on, perhaps even for many years, but never again must it be allowed to claim the moral high ground.

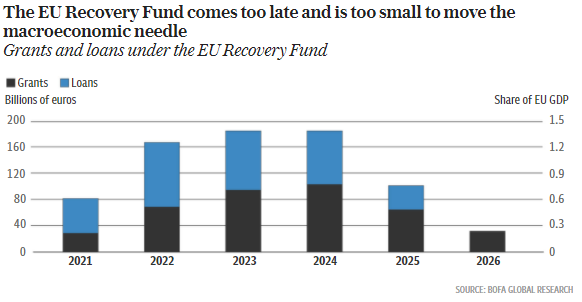

Will the much-vaunted EU Recovery Fund save the union from the coming disaster? Not a chance. Ambrose Evans-Pritchard explains why.

The EU’s €750bn Recovery Fund is more publicity stunt than macro-stimulus. Half comes in the form of loans that mostly displace borrowing that would have happened anyway. The €390bn in actual grants is spread over five years between 27 countries. Italy will receive just 0.7pc of GDP a year once its own payments as an EU net contributor are stripped out. The sums arriving this year are just a trickle…Once again, the ECB will have to paper over trouble with funny money. It will have to continue its disguised (or at least denied) monetary-fiscal rescue of southern European governments. Should it cease to do so - or even hint at an end to bond purchases - markets will take instant flight. The implicit sovereign bankruptcy of Italy will become explicit. Debt restructuring will be on the table. That will unleash the political demons.

Due to the vaccine debacle, the EU will suffer its virus-exacerbated recession for longer than necessary. Even after it eventually emerges from the Covid crisis, there is still no hope of solving the north-south divide and the south’s unpayable debts. How long will the Germans permit the ECB to buy Italian government bonds knowing that nation has no ability to retire them? The EU is structurally flawed. The entrenched Brussels bureaucrats will never willingly give up their powers and privileges but Germany will not continue to underwrite them. There will be a day of reckoning.

When the crisis comes Brussels will argue that it needs more power, especially the power to tax as a central government and to control the outlays. We doubt that the northern states will ever agree to such a complete transfer of national power to the EU. The UK saw the handwriting on the wall and prudently made its exit.

Bitcoin Update

With much fanfare, Elon Musk announced that Tesla bought $1.5B of Bitcoin and may agree to be paid for cars with Bitcoins. Almost immediately, several banks, credit card companies and PayPal announced their intention to accept or store Bitcoins. Why this sudden surge of interest in Bitcoins? Perhaps the reason is to try to put Bitcoins into common usage before governments act on their threats to regulate it.

We recently wrote that there are serious threats to digital currencies. These come from governments that have a vested interest in maintaining their monopoly on currencies and they are not expected to tolerate anyone or anything that seriously threatens that monopoly. We cautioned that governments could at any time put regulations into force that could dramatically affect the value of cryptocurrencies. We said that their justification for doing so will be the argument that criminals and terrorists use them. It did not take long for the first shoe to drop and for the exact justification we cited.

The US Treasury Department posted for comment a proposed regulation that would require all entities dealing in digital currencies to identify each holder and confirm the legitimacy of his or her source of funds. In the world of banking and securities this is called the duty to “Know Your Customer.” These organizations are obligated to engage in due diligence in investigating their customers before opening an account. Should this regulation go into effect, all Bitcoin owners who transact business outside of the blockchain would have to be identified and each of their transactions would be subject to scrutiny with compelled reporting to authorities should they have reason to suspect there is something untoward about a given transaction. These reports are called Suspicious Activity Reports. They are filed with the Treasury Department. This regulation would eliminate all privacy associated with digital currencies held in banks, securities accounts, credit card accounts and other payment forums (e.g., PayPal) and subject every transaction to scrutiny and reporting to the authorities.

Furthermore, at a US Senate hearing, Janet Yellen expressed her concerns that cryptocurrencies are used to finance illegal activities. “Cryptocurrencies are a particular concern, I think many are used — at least in a transactions sense — mainly for illicit financing. And I think we really need to examine ways in which we can curtail their use” (emphasis added). As the head of the Treasury Department she is well-positioned to bring about restrictive regulations. The ECB’s Christine Lagarde has also called for global regulation of Bitcoin and proposed a Know Your Customer requirement. If cryptos become regulated by governments, one of their principal raisons-d’etre would be lost. This will be an interesting battle between the people, who seek freedom and protection from the government, and the government that seeks to deny them that freedom and protection.

A New Beginning for the US?

With Joe Biden now sworn in as the US president the issue is whether there will be any meaningful changes in our form of governance. Early signs suggest that there will not. On October 15, 2020, just two weeks before the election, candidate Biden was interviewed and said:

“I have this strange notion. We are a democracy. Some of my Republican friends, and some of my Democratic friends occasionally say, ‘well if you can’t get the votes, by executive order you’re going to do something. You can’t do it by executive order, unless you’re a dictator. We’re a democracy, we need consensus.”

During Trump’s first weeks in office he signed four executive orders, Obama signed five, GW Bush signed none and Clinton signed one. Biden? We stopped counting at forty-two. His supporters will contort themselves trying to find ways to justify his hypocrisy, but Biden’s own words now define him. He is acting like a dictator.

What about the “unity and consensus” we heard so much about at the inauguration? He wants to pass a $1.9 trillion aid package. With great televised fanfare he met with Republicans who suggested several compromises. The word is that the Democrats will ram through their full plan without any Republican support via the reconciliation process (a scheme to avoid the 60% vote requirement). If you are one of those holding your breath and waiting for the new era of consensus and unity, it is time to exhale. We learn the lesson once again to ignore what politicians say and watch what they do.

© All rights reserved 2021

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance.